Performance

Support for your Double Materiality Assessment

Let us provide you with professional support in carrying out your materiality analysis in accordance with the ESRS standards. Together, we will develop a process that will enable you to carry out your materiality analyses simply and easily in accordance with the requirements of the Corporate Sustainability Reporting Directive (CSRD).

Our experts are on hand to provide you with professional support for your materiality assessment. Give us a call or make an appointment for a personal consultation.

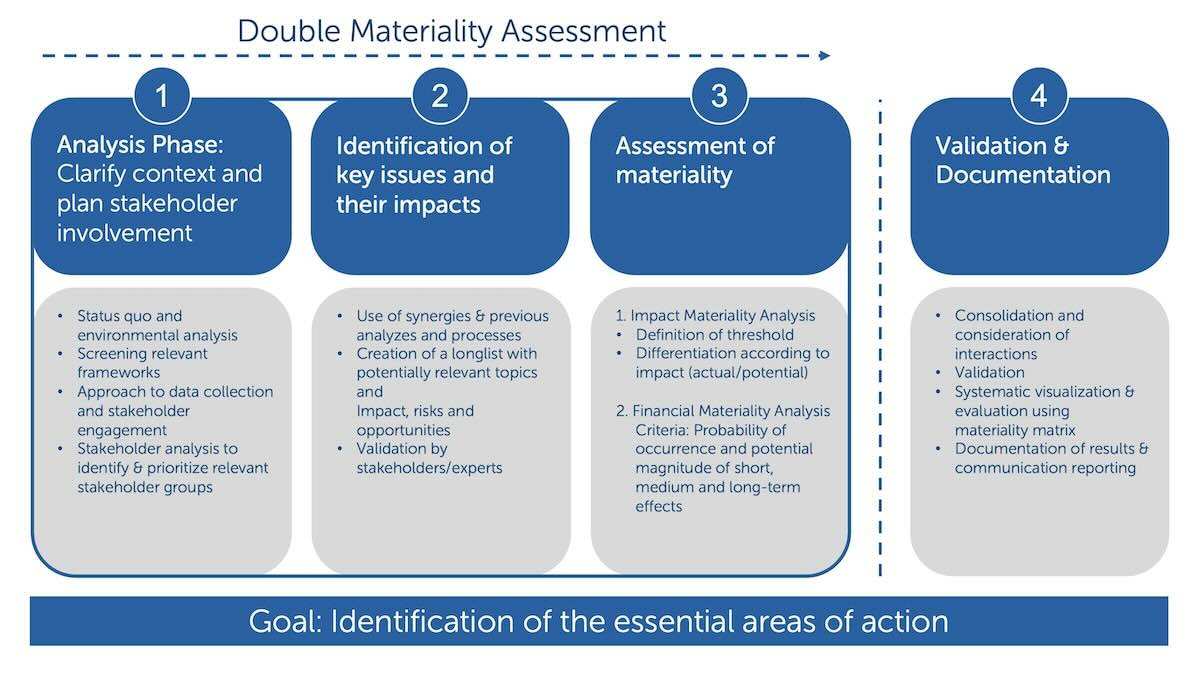

Implementation of the double materiality assessment

Determining relevant sustainability aspects, identifying and involving relevant stakeholders, prioritizing fields of action and finally determining the material sustainability aspects that must be reported in the CSRD report are the central objectives of the double materiality analysis. Which sustainability topics must be reported in accordance with the ESRS depends on the individual importance of the topic for the respective company. In future, companies will decide independently which topics to report on the basis of a previously conducted materiality analysis.

This is how we support you with your specific sustainability issues

The CSRD emphasizes dual materiality, which includes both financial and non-financial factors. This approach enables a comprehensive view of sustainability aspects and helps companies to focus their reporting on relevant topics that are important both for the company's results and for the needs of stakeholders and society.

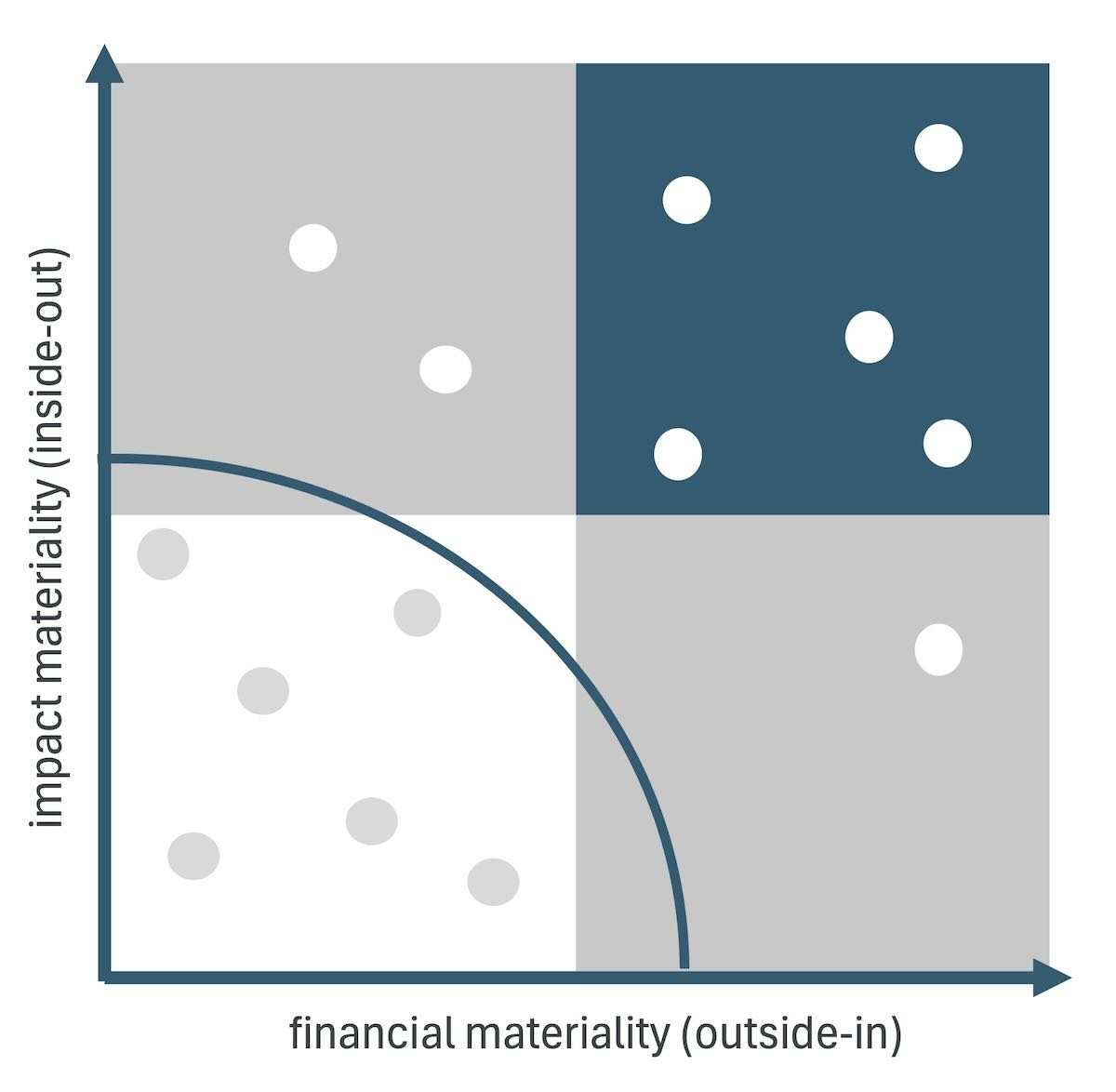

Relevant topics are identified using a materiality matrix, for example.

The analysis shows to what extent and with what intensity the company has to deal with the topics. The following perspectives are used to determine whether an issue is material and therefore reportable:

- Inside-out perspective (impact materiality/significant impact): This looks at the impact that the company's business activities and value chain have on people and the environment. Aspects are identified here that are relevant for the stakeholder groups affected and that can influence the reputation and long-term sustainability of the company. Both positive and negative impacts are considered here.

- Outside-in perspective (financial materiality): The impact of sustainability risks on the company's financial performance and economic success is assessed. It looks at how sustainability aspects represent a risk or an opportunity for the company that has a financial impact on the company in the short, medium or long term.

Advantages of the materiality assessment

- Limitation of data points: Over 1000 data points are reduced to a more manageable number through the materiality analysis. Only what is material needs to be reported.

- Focused budget utilization: Through clear priorities, limited budgets can be concentrated on the really important issues, which increases the effectiveness of sustainability management.

- Targeted measures along the value chain: Insights into whether an issue affects the entire value chain or only certain areas such as the supply chain provide concrete starting points for management. This leads to a clear allocation of responsibilities within the company, whether in purchasing, product development, production or sales.

- Stakeholder feedback: A survey of a large number of stakeholders provides statistically sound insights into which topics are considered material by which groups. This information is valuable for the development of targeted solutions.

Our experts are on hand to provide you with professional support for your materiality assessment. Give us a call or make an appointment for a personal consultation.

Sustainability report

Get professional support with your sustainability reporting based on the European Sustainability Reporting Standards (ESRS). Together, we will establish a reporting process that will enable you to prepare your own reports simply and easily in accordance with the requirements of the Corporate Sustainability Reporting Directive (CSRD).

Sustainability consulting

Customers and investors are increasingly demanding that companies adopt sustainable and social corporate governance. This is now also supported by law. But what exactly do these market requirements mean and how can they be met? We support you on the path to sustainable transformation.